All Categories

Featured

Table of Contents

Ensure any representative or company you're considering purchasing from is accredited and economically stable. To validate the Texas certificate condition of a representative or firm, call our Assistance Line at 800-252-3439. You can also utilize the Company Lookup feature to find out a company's economic score from an independent ranking company.

Right here at TIAA, we allow proponents of fixed annuities and the ensured lifetime earnings they provide in retired life. Set annuities provide retired people better liberty to invest, they lower the threat of retired people outlasting their financial savings, and they might even aid senior citizens stay much healthier for longer.1 We don't chat almost as much about variable annuities, despite the fact that TIAA originated the very first variable annuity back in 1952.

Highlighting the Key Features of Long-Term Investments Key Insights on Your Financial Future What Is Annuities Variable Vs Fixed? Benefits of Choosing the Right Financial Plan Why Fixed Vs Variable Annuity Is Worth Considering How to Compare Different Investment Plans: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Risks of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Fixed Income Annuity Vs Variable Annuity Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Variable Annuity Vs Fixed Annuity A Beginner’s Guide to Deferred Annuity Vs Variable Annuity A Closer Look at How to Build a Retirement Plan

Cash allocated to a variable annuity is spent in subaccounts of different possession classes: stocks, bonds, money market, and so on. Variable annuity efficiency is linked to the hidden returns of the chosen subaccounts. Throughout the build-up phasepreretirement, in various other wordsvariable annuities are similar to common funds (albeit with an insurance policy wrapper that impacts the cost yet can include some defense).

That conversion is referred to as annuitization. Participants are under no commitment to annuitize, and those who do not generally make withdrawals just as they would with a common fund. Senior citizens that depend on a withdrawal strategy run the danger of outlasting their cost savings, whereas those that choose for lifetime revenue understand they'll get a check every montheven if they live to 100 or beyond.

Variable annuities usually have an assumed financial investment return (AIR), usually between 3% and 7%, that identifies a standard regular monthly settlement. If the financial investment efficiency is higher than the AIR, you'll obtain even more than the common payment. If the investment efficiency is much less, you'll get less. (As we said, variable annuities can be intricate, so speak with your TIAA financial advisor for details.) If you pick single-life annuitization, repayments end when you die.

For better or for worse, looking for a variable annuity is a bit like looking for new vehicle. You start checking out the base design with the basic trim. Yet include all the special features and optionssome you require, some you possibly do n'tand what started out as a $40,000 sedan is currently closer to $50,000.

Some also have options that boost regular monthly payouts if you come to be handicapped or require long-lasting treatment. Eventually, all those bonus (additionally recognized as riders) add upso it's crucial to go shopping for variable annuities with a monetary business and monetary advisor you trust.

With a dealt with annuity, the month-to-month payment you obtain at age 67 is generally the same as the one you'll access 87which would certainly be fine if the cost of food, housing and healthcare weren't climbing. Repayments from a variable annuity are more probable to equal rising cost of living due to the fact that the returns can be connected to the supply market.

Analyzing Strategic Retirement Planning A Closer Look at Fixed Vs Variable Annuity What Is Variable Annuity Vs Fixed Indexed Annuity? Benefits of Fixed Income Annuity Vs Variable Growth Annuity Why Fixed Indexed Annuity Vs Market-variable Annuity Matters for Retirement Planning How to Compare Different Investment Plans: Explained in Detail Key Differences Between Indexed Annuity Vs Fixed Annuity Understanding the Risks of Fixed Income Annuity Vs Variable Growth Annuity Who Should Consider What Is Variable Annuity Vs Fixed Annuity? Tips for Choosing Variable Vs Fixed Annuities FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Annuities Fixed Vs Variable A Beginner’s Guide to Fixed Vs Variable Annuities A Closer Look at How to Build a Retirement Plan

As soon as annuitized, a variable annuity becomes a set-it-and-forget-it source of retired life earnings. You don't require to decide just how much to withdraw each month because the choice has actually currently been madeyour repayment is based on the performance of the underlying subaccounts. This is practical since people are more susceptible to money errors as they age.

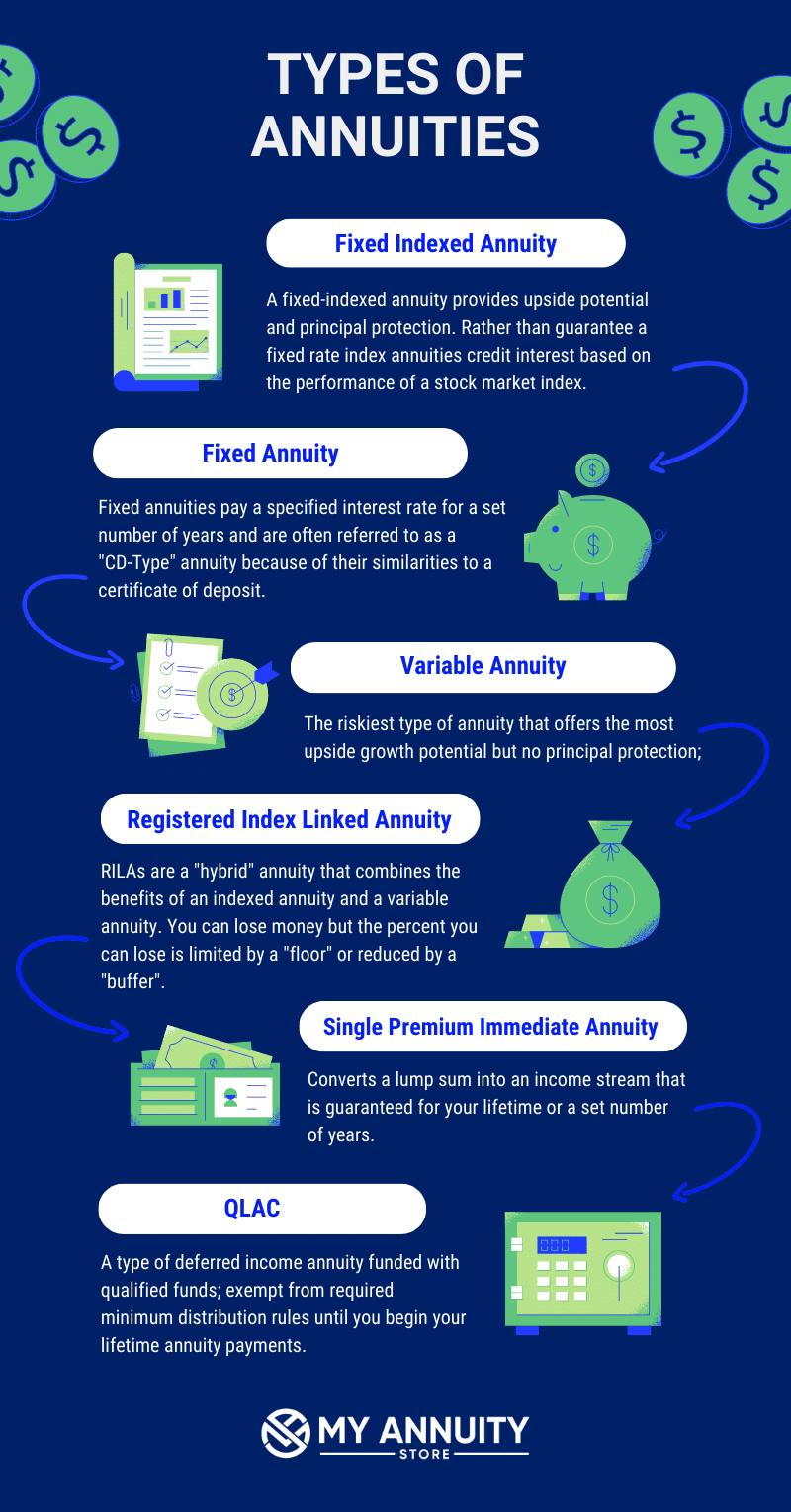

While they provide the capacity for higher returns, they include greater danger as the principal is not secured. In addition, rate of interest can be shed due to inadequate performance.: These provide guaranteed settlements, providing stability and predictability. Your principal is secured, and you get a fixed rate of interest over a specified period.

The interest is secured, making certain that your returns continue to be secure and untouched by market volatility.: These are hybrids supplying a minimal surefire passion rate with the capacity for greater returns linked to a market index, such as the S&P 500. They incorporate components of dealt with and variable annuities, supplying an equilibrium of threat and incentive.

VariableAnnuityFixed IndexAnnuityFixedAnnuityYesYesYesYesYesYesYesYesYesYesYesNoYesYesYesYesYesYesYesYesYesYesYes: This is a kind of dealt with annuity where you obtain payments at a future day instead of immediately. It's a way to defer your earnings up until retirement to take pleasure in tax benefits.: This is a variable annuity where the earnings is deferred to a later date. The amount you'll receive depends on the efficiency of your chosen financial investments.

Allow's speak concerning Fixed Annuities versus variable annuities, which I like to speak concerning. Currently, please note, I do not offer variable annuities. I sell legal warranties.

Understanding Financial Strategies Key Insights on Your Financial Future Defining Annuity Fixed Vs Variable Features of Smart Investment Choices Why Choosing the Right Financial Strategy Can Impact Your Future How to Compare Different Investment Plans: How It Works Key Differences Between Annuities Fixed Vs Variable Understanding the Rewards of Long-Term Investments Who Should Consider Fixed Interest Annuity Vs Variable Investment Annuity? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Retirement Income Fixed Vs Variable Annuity A Beginner’s Guide to Annuities Variable Vs Fixed A Closer Look at How to Build a Retirement Plan

All right, I'm mosting likely to explain annuities. Who better to describe annuities than America's annuity agent, Stan The Annuity Man. Allow's chat concerning variable annuities. Variable annuities, basically, in English, in Southern, mutual funds covered with an insurance policy wrapper. And for whatever factor, they do not call them common funds in the annuity industry.

I will call them shared funds since guess what? Variable annuities sold out in the hinterland are amongst the most popular annuities. Currently, variable annuities were placed on the earth in the '50s for tax-deferred development, and that's amazing.

I recognize, yet I would claim that in between 2% to 3% typically is what you'll find with a variable annuity fee for the plan's life. Every year, you're stuck starting at minus 2 or minus three, whatever those costs are.

I suggest, you can attach income bikers to variable annuities. We have actually located that revenue riders connected to repaired annuities generally supply a greater legal warranty.

And when again, please note, I don't sell variable annuities, but I know a lot concerning them from my previous life. There are no-load variable annuities, which means that you're liquid on day one and pay a very small reduced, low, reduced cost.

If you're going to state, "Stan, I have to acquire a variable annuity," I would certainly state, go acquire a no-load variable annuity, and have a professional cash manager handle those different accounts inside for you. But when again, there are restrictions on the options. There are limitations on the choices of shared funds, i.e., different accounts.

Decoding How Investment Plans Work A Closer Look at Annuities Fixed Vs Variable Defining the Right Financial Strategy Benefits of Choosing the Right Financial Plan Why Choosing the Right Financial Strategy Can Impact Your Future How to Compare Different Investment Plans: Explained in Detail Key Differences Between What Is A Variable Annuity Vs A Fixed Annuity Understanding the Key Features of Long-Term Investments Who Should Consider Fixed Vs Variable Annuities? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Fixed Vs Variable Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

Let's talk about Fixed Annuities versus variable annuities, which I enjoy to talk regarding. Now, disclaimer, I do not offer variable annuities. I sell contractual assurances.

All right, I'm mosting likely to clarify annuities. That better to describe annuities than America's annuity agent, Stan The Annuity Male. Allow's discuss variable annuities. Variable annuities, basically, in English, in Southern, mutual funds wrapped with an insurance coverage wrapper. And for whatever reason, they don't call them shared funds in the annuity industry.

I will call them mutual funds since hunch what? They're common funds. That's what they are. Variable annuities offered out in the hinterland are amongst the most popular annuities. Now, variable annuities were placed on the planet in the '50s for tax-deferred development, and that's fantastic. What they've transformed right into, unfortunately, is very high-fee products.

I understand, yet I would certainly claim that in between 2% to 3% normally is what you'll discover with a variable annuity charge for the policy's life. Every year, you're stuck starting at minus 2 or minus three, whatever those costs are.

Now, they're not terrible products. I mean, you can connect earnings bikers to variable annuities. We have found that income motorcyclists connected to taken care of annuities typically provide a greater contractual guarantee. But variable annuities are also good to be a true sales pitch. Market growth, and you can attach warranties, et cetera.

And once again, please note, I don't offer variable annuities, yet I know a lot about them from my previous life. There are no-load variable annuities, which suggests that you're liquid on day one and pay a very minor reduced, reduced, low charge. Usually, you manage it on your own. Some no-load variable annuities are out there that experts can handle for a cost.

Analyzing Strategic Retirement Planning Key Insights on Your Financial Future What Is the Best Retirement Option? Features of Fixed Vs Variable Annuities Why Choosing the Right Financial Strategy Is a Smart Choice Indexed Annuity Vs Fixed Annuity: How It Works Key Differences Between Fixed Vs Variable Annuity Understanding the Rewards of Fixed Vs Variable Annuity Pros Cons Who Should Consider Variable Vs Fixed Annuities? Tips for Choosing Deferred Annuity Vs Variable Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Annuity Fixed Vs Variable A Closer Look at Fixed Vs Variable Annuity Pros And Cons

If you're going to state, "Stan, I have to buy a variable annuity," I would state, go purchase a no-load variable annuity, and have a specialist money supervisor manage those different accounts internally for you. Once again, there are constraints on the options. There are constraints on the choices of common funds, i.e., different accounts.

{kind=link}

Table of Contents

Latest Posts

Understanding Financial Strategies A Comprehensive Guide to Fixed Income Annuity Vs Variable Annuity Defining the Right Financial Strategy Benefits of Choosing the Right Financial Plan Why Choosing th

Understanding Tax Benefits Of Fixed Vs Variable Annuities A Closer Look at Fixed Annuity Or Variable Annuity What Is Annuities Fixed Vs Variable? Pros and Cons of Variable Annuities Vs Fixed Annuities

Analyzing Strategic Retirement Planning Everything You Need to Know About Financial Strategies Defining What Is A Variable Annuity Vs A Fixed Annuity Pros and Cons of Various Financial Options Why Cho

More

Latest Posts